Sourcing Shift Insights:

Electrical & Electronics Products

Imports of Electrical and Electronics products (including small and large appliances, HVAC, lighting, electrical tools, and audio-visual equipment) grew by 5.4% for electrical and 1.7% for electronics by weight between 2019 and 2024. This growth was driven by tariff-induced diversification from China toward emerging hubs such as Mexico, Vietnam, Canada, and India. While these regions offer cost advantages, quality risks persist, with defect rates in alternative hubs exceeding 30–50%.

Key Trends for Electrical and Electronics Products Sourcing

% Overall Decline in China Dependency

China’s share of U.S. electrical and electronics products imports fell by 15.3% since 2019, with notable double-digit declines in:

- Power tools: –27.7%

- Lighting: –17.3%

- Audio-visual equipment: –16.8%

- Small domestic appliances: –14.1%

High-Exposure Categories

- Small domestic appliances remain 61.6% China-sourced despite growth in Mexico and Vietnam.

- Lighting imports still rely 43.3% on China, while Vietnam and Canada together account for 11.2%.

- Vietnam emerges as a fast-growing hub for EE products, posting an 8.8% CAGR.

Category Spotlight: Audio-Visual (AV) Equipment

The United States has been a key market for audio-visual (AV) equipment, with much of it sourced from China. Recently, there is growing interest in diversifying the supply chain to reduce dependence on Chinese-made AV products. This shift is driven by trade tensions, intellectual property concerns, and efforts to boost domestic manufacturing capacity.

China leads globally in producing electronic components and finished AV products, offering competitive prices and strong logistics. Moving away from this established supply chain is complex and requires investment in alternative sourcing, production, and supply chain management.

- U.S. market heavily sourced from China

- Rising interest in supply chain diversification

- Drivers: trade tensions, IP protection, domestic capacity

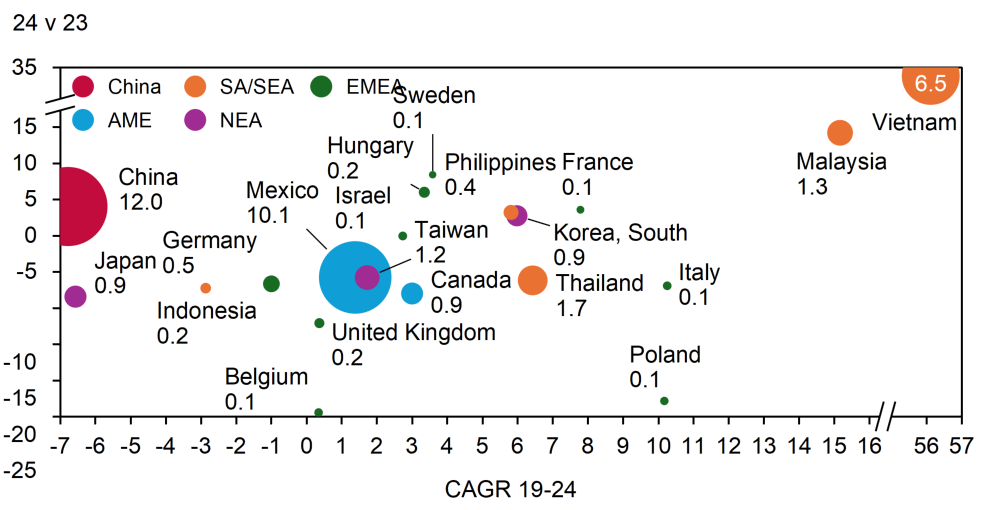

Sourcing Shifts

- China remains a strong U.S. AV trade partner at $12.0B, but trade volume has declined at a -7% CAGR from 2019 to 2024.

- Mexico, Vietnam, and Thailand show steady growth as alternative U.S. AV suppliers.

- Maintaining product quality and reliability is critical, as AV equipment is mission-critical for many users.

- Tariffs, trade policies, and regulatory changes impact cost and availability, complicating sourcing decisions.